In this post, we will see why the 50-year mortgage won’t solve the housing affordability crisis. But first, our disclosure:

50-Year Mortgage: Is This A Joke?

When I first heard that the Trump administration was floating the idea of a 50-year mortgage, I laughed. I honestly thought it was a joke.

It reminded me of the 7-minute abs scene from There’s Something About Mary. In the scene, a hitchhiker pitches Ben Stiller’s character on “7-minute abs” to rival the very real “8-Minute Abs” franchise. He’s so proud of it, until Ben Stiller throws cold water on the idea when he points out that someone else can just come up with 6-minute abs.

That’s kind of how the 50-year mortgage feels to me, but in reverse. If 30 years wasn’t enough and now 50 is supposed to be the magic fix, what’s next? A 75-year mortgage? A 100-year mortgage? A loan you literally pass down to your kids like a family heirloom?

I’ll admit, 50-year mortgages aren’t totally out of left field. FDR and the New Deal gave us 30-year mortgages for similar reasons. But that doesn’t mean we need 50-year mortgages.

On paper, the idea looks good. Stretch out the payments, make the monthly payments smaller, and more people can “afford” a house. Except that is not really the case.

Lowering the monthly payment will increase demand. In turn, prices rise, and buyers end up exactly where they started, just with a longer debt sentence.

Before we jump into why the 50-year mortgage won’t solve the home affordability crisis, let’s see how we got into this mess in the first place.

The Main Culprits: The Great Recession & COVID

The Great Recession of 2008 did more damage to the housing market than just increasing foreclosures. It sent demand plummeting, causing home prices to drop off a cliff. The lack of demand and plummeting home prices caused new constructions to dry up faster than a desert in the summer. Mortgage rates followed right along, dropping to record lows.

Eventually, an improving economy along with ridiculously low mortgage rates fueled housing demand once again. And when it did, the housing market came back with a vengeance.

It was brutal. I was looking for my first home during this time, and it took me over 3 years to finally close on a home. I lost so many offers to buyers bidding $20K, $30K, or even more than $50K over the asking price! Granted, we are talking about the Boston housing market, but still.

And it has only gotten worse since the COVID pandemic.

COVID, Stimulus, Mortgage Rates, Oh My!

Then, along came the COVID-19 pandemic with its lockdowns, stimulus checks, and even lower mortgage rates. It was like pouring gasoline on fire.

Demand went through the roof, and the lack of supply sent home prices up nearly 20% in a single year, not once, but twice! Then inflation came roaring back, and mortgage rates nearly doubled overnight. It was the perfect storm! Salaries just couldn’t keep up.

Fast forward to today, and we are still facing supply shortages, and homeowners who are lucky enough to have a ridiculously low mortgage rate aren’t selling. I know I’m not.

Given current home prices and mortgage rates, my house would cost me nearly twice as much if I were to buy it today. That’s why most people with a low-rate mortgage are not selling. Instead, they are adding on to their homes rather than buying a bigger, more expensive one at more than double their current mortgage rate.

A 50-year mortgage won’t fix home affordability, and here’s why:

1. Disappearing Lower Payments

When I go online, I see people comparing the monthly payments of a 30-year fixed mortgage with a 50-year fixed mortgage, using an example like the one below;

Monthly payments on a $400K mortgage at a 6% interest rate without PMI (rounded):

- 30-year mortgage: $2,400

- 50-year mortgage: $2,100

Looks pretty nice on paper, “saving” around $300 a month. The issue: On what planet would a 50-year mortgage have the same rate as a 30-year mortgage? That is highly unlikely. You probably have better odds of winning the lottery.

Instead, a 50-year mortgage would likely have a higher interest rate, as banks take on more risk the longer the loan term. It’s why 15-year mortgages tend to have lower interest rates than 30-year mortgages.

If I were a betting man, I would bet that a 50-year mortgage would be 50 to 100 basis points higher than a 30-year mortgage. So, instead of a 50-year mortgage having a 6% rate like in our example above, odds are it would be closer to 6.5% to 7%.

Here is what the above comparison looks like, assuming a 6.5% rate on the 50-year mortgage (rounded):

- 30-year mortgage at 6%: $2,400

- 50-year mortgage at 6.5%: $2,250

And here is the comparison, assuming a 50-year mortgage at a 7% rate:

- 30-year mortgage at 6%: $2,400

- 50-year mortgage at 7%: $2,410

As you can see, the lower payment disappears when the rate on a 50-year mortgage approaches 100 basis points (1%) above the rate of a 30-year mortgage. From here, it only gets worse as you factor in interest.

2. 50 Years Of Interest

A 50-year mortgage might modestly lower your monthly payment compared to a 30-year mortgage, but only because you’re stretching the loan across an extra 20 years. However, those extra 20 years come with a hefty price tag. When I say hefty, I mean a bone-crunching, soul-crunching boulder of interest payments.

Let’s see how much that extra 20 years will cost you, using our example from above of a $400K mortgage at a 6% interest rate (rounded):

- 30-year mortgage at 6% total interest paid: $463,350

- 50-year mortgage at 6% total interest paid: $863,370

Those 20 extra years cost you $400,000 more in interest! In this example, the total cost of borrowing $400,000 for a home is $1,263,371.51 with a 50-year mortgage, compared to $863,352.76 with a 30-year mortgage. That is triple the original amount!

But wait! Remember, odds are a 50-year mortgage will have a higher interest rate than a 30-year mortgage. So let’s revisit the 6.5% and 7% examples from earlier. If we do, we get the following total interest payments:

At 6.5%:

- 30-year mortgage at 6% total interest paid: $463,350

- 50-year mortgage at 6.5% total interest paid: $952,920

At 7%:

- 30-year mortgage at 6% total interest paid: $463,350

- 50-year mortgage at 6.5% total interest paid: $1,044,050

That’s over $1 million in interest! How is this affordable?

These are only examples, but math is still math, and the bottom line is that those extra 20 years don’t come cheap.

3. Takes Forever To Build Equity

I can already hear many people screaming at their computer, arguing that no one holds the original mortgage to the full term. That’s true.

The average time someone holds a mortgage is around 10 years, give or take. But in most cases, it’s not because they paid off their mortgage. It is because the homeowner either refinances into another mortgage or buys another house.

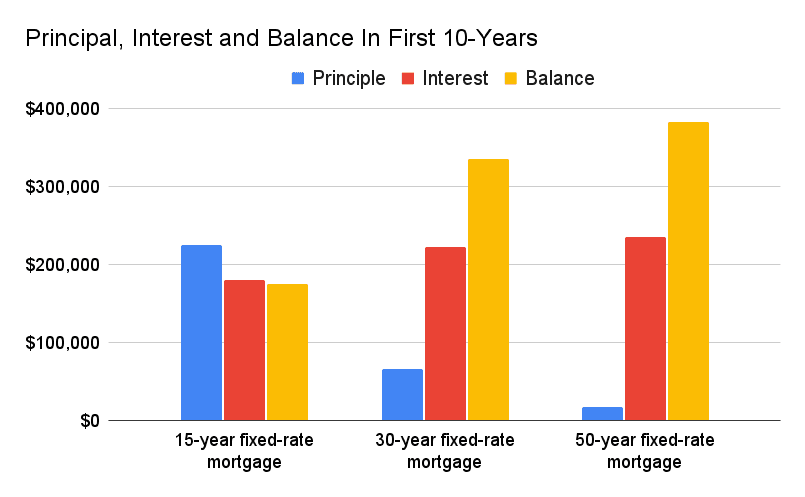

The downside is that in the first 10 years of a fixed-rate mortgage, a larger portion of your payments goes toward interest rather than principal. This process is known as amortization. With a 50-year fixed-rate mortgage, that means much more of your earlier payments will go toward interest compared to a 15-year or 30-year fixed-rate mortgage.

How much?

Let’s have a look using our example of a $400K home at a 6% mortgage.

Below is a chart showing the total amount paid toward principal and interest in the first 10 years of the mortgage (rounded):

| Mortgage | Principal | Interest | Balance |

|---|---|---|---|

| 15-year fixed-rate mortgage | $225,405 | $179,650 | $174,600 |

| 30-year fixed-rate mortgage | $65,260 | $222,530 | $334,740 |

| 50-year fixed-rate mortgage | $17,310 | $235,370 | $382,690 |

The chart above shows that after a decade of making payments on a $400,000, 50-year fixed-rate mortgage, you would still owe $382,690. Your equity in the house would have only grown $17,300, not counting any appreciation in the home’s value. In other words, after 10 years, you barely left the starting line.

If interest rates go down and you decide to refinance into a lower-rate 50-year mortgage, it’s like starting all over again. If you choose to refinance into a 30-year fixed-rate mortgage instead, you can’t escape the fact that you just spent a decade paying $235,370 in interest on the original loan over the past decade.

Setting the Record Straight on Mortgage Arbitrage

Before we look at the remaining issues with the 50-year mortgage, I want to address mortgage arbitrage.

Mortgage arbitrage is when a homeowner chooses to invest money they could have put toward paying off a low-rate mortgage more quickly.

For example, if your mortgage rate is 3% and you invest in an S&P 500 index fund that averages a 10% return, then your spread is 7%. Given enough time, the investment will compound and grow much faster than your equity and home appreciation.

Many people on social media are claiming the 50-year mortgage is superior to a 15- or 30-year mortgage solely because it results in lower monthly payments, allowing homebuyers to invest the difference. I don’t agree with that position.

As we have seen, odds are the interest rate on a 50-year mortgage will be higher than on a 15- or 30-year mortgage, eliminating much of those monthly savings. Any remaining difference in monthly payments will be eaten up by property taxes (they go up almost every year!) and maintenance and repair costs. Then there is private mortgage insurance (PMI).

If a homebuyer is taking out a 50-year mortgage, I would wager they are not putting down a full 20%. This means they will likely pay hundreds of dollars in private mortgage insurance (PMI) each month.

The problem: You can’t get rid of PMI until you have 20% equity in the property.

They’d better hope the property appreciates quickly, since so little will be going to principal, or they can be looking at almost 20 years of PMI.

Lastly, mortgage rates have historically averaged around 7%. Those ultra-low mortgage rates around COVID were an anomaly. There are very few investments that can beat 7% once you factor in all of the above costs.

4. The Debt Can Outlive You

According to the National Association of Realtors, the median age of a first-time homebuyer is now a record high of 40. I feel the pain, as I fit this statistic to a tee. To put this number in perspective, back in the 1980s, the median age of first-time homebuyers was around 29.

It’s bad enough for a 40-year-old who takes out a 30-year mortgage, as they won’t pay it off until they are 70. If they go with a 50-year mortgage, they won’t pay it off until they are 90, unless they pay extra toward the principal!

That means, with a 50-year mortgage, a big portion of someone’s retirement income will need to go toward paying off their mortgage for decades after they retire. Of course, a homeowner can always sell or refinance, but as we saw above, it may not be much cheaper. Sadly, their family may be stuck paying off the balance.

That is not affordability. That is debt, masquerading as a generational asset.

5. Increases Demand Without Supply

Ultimately, a 50-year mortgage will increase demand and inflate home prices. It will bring new buyers into the market chasing a limited number of homes, while longer terms will give the illusion of “affordability” while pushing home prices higher. It is exactly what we have seen with car loans.

Car dealers have extended the car loan to 84 months so more people can afford the monthly payments. That has not lowered car prices. It’s just a financial gimmick where those who make out the most are the banks, earning interest on the loans.

Unless we get serious about building new homes, no amount of financial gimmicks will solve the affordability crisis.

A 50-year Mortgage: The Bottom Line

The bottom line is that a 50-year mortgage does nothing to improve affordability in the housing market. Instead, it increases the total interest paid to lenders, raises home prices, and potentially locks buyers into a generational debt trap.

The truth is, we don’t need longer mortgages. We need more homes that people can afford.

The problem is that increasing affordability is no small task. It would require tackling a number of issues, including:

- Increasing the housing supply

- Changing zoning laws

- Increasing Income/wages

- Addressing the impact of private equity in residential housing.

Until these issues are fixed, financing gimmicks like a 50-year mortgage will only prolong the problem, not fix it.

{kind=link}